STEM I

Course Description

STEM with Science and Technical Writing is an immersive course

into the world of STEM and scientific writing. This course consisted

of a 7-month-long Independent Research Project during the beginning

of the Junior Year where students researched and investigated a topic

of their choice to present at the final school-wide fair in February,

Assessing the Correlation Between Genetic Predisposition and

Health Insurance Rates

Overview

Health Insurance Companies may look at rates of genetic

mutations associated with higher risks of health conditions to

determine their premiums. To assess this possibility, the correlation

between the rates of 20 health conditions varying in their degree of

genetic heritability and health insurance rates was assessed.

Abstract

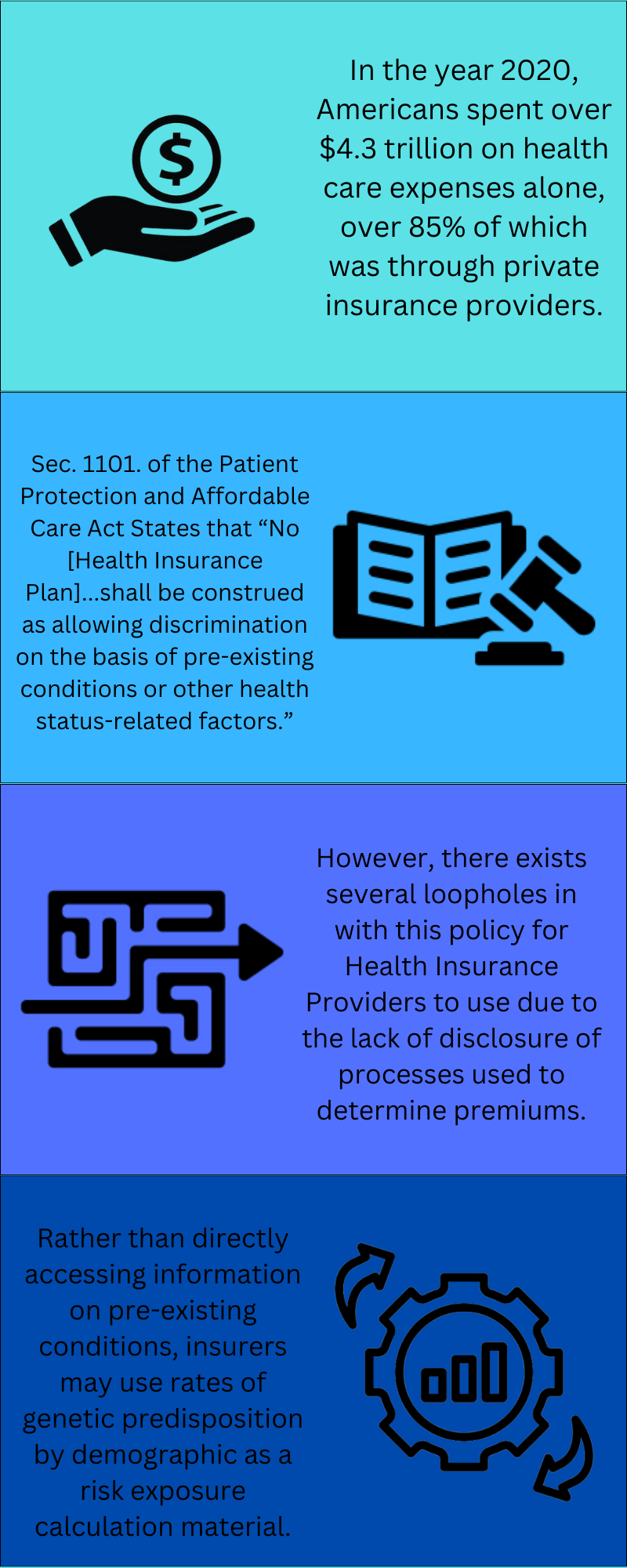

Health insurance is costly; Americans spent over $4.3 trillion

on healthcare expenses in 2020 alone, with over 85% through private

insurance providers (Center for Medicare and Medicaid Expenses,

2020). In 2010, The Patient Protection and Affordable Care Act

restricted health insurers' ability to deny and raise rates due to

pre-existing medical conditions. However, it was challenging to

enforce this section of the act because very little information is

known about how insurance providers determined their rates. This

study aimed to help resolve this knowledge gap by conducting a

correlative study between rates of genetic predisposition and health

insurance costs. Health insurance data was collected using public

marketplace databases, and information on rates of health conditions

was collected. Then, a Pearson Correlation was run on the two

datasets. The result was a Pearson Coefficient of r = 0.1198 for all

conditions and a statistic of r = 0.1464 among genetic conditions.

This result offered significant evidence that health insurance

companies used information on genetic predisposition to determine

their rates. This conclusion has significant implications for both

the healthcare and genetic testing industry. The information provided

by this study could be considered by clients interested in proceeding

with genetic testing, as being informed of the risk factors

associated with health insurance rates resulted in doing so.

Additionally, the study provided evidence for conducting a future

study using genetic mutation rates rather than incidence rates, which

would be used to rephrase legislation and terminology in the

Affordable Care Act.

Research Proposal

My full research proposal can be read here.

Phrase 1

What information do health insurance providers look at when

determining their rates?

Phrase 2

This study hypothesized that health insurance companies look at

genetic information to determine their rates.

Background

The Patient Protection and Affordable Care Act of 2010 (United

States, 2010), also commonly known as Obamacare, has been known to be

a rather controversial policy by many Americans. Nevertheless, it has

had many undeniable impacts on the medical industry and health

insurance providers. The subsection of the law regarding policy

relating to pre-existing health conditions is often considered to be

one of the most, if not the most impactful part of the act

(Kirzinger, 2022). The section states that no individual with a

pre-existing medical condition may be refused health insurance

because of their pre-existing medical condition. Although aspects of

these policies vary from state to state (Kominski, 2017), the

particular section mentioned above remains applicable on a national

level. However, insurance costs remain significantly expensive for

Americans across the nation, and these costs are only growing. In

2021, Americans spent about $4.3 trillion on health care expenses –

nearly 85% of these expenses being into Private Insurance Providers-

meaning the average American spends approximately $10,976 a year on

health insurance. Although the Affordable Care Act (ACA) aimed to

combat these costs, in response to the policies put into place by the

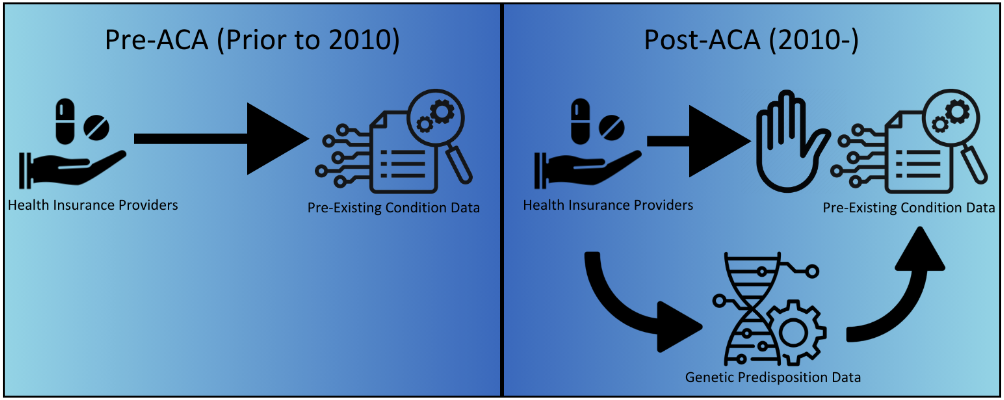

ACA, health insurance agencies have several methods to combat these

restrictive policies by taking advantage of loopholes in the

legislation. One such loophole exists due to the poor definition of

the phrase “refusing health insurance based on pre-existing medical

conditions” (United States, 2010). Because of the wording of this

section, although it is illegal for insurance agencies to directly

reject someone due to a pre-existing medical condition, they can

instead determine the probability that someone has an existing

medical condition or will be likely to develop one in the future

based on information on their demographics. This process will provide

the insurance agencies with a reasonable estimate of whether a

potential client has a pre-existing medical condition without needing

to directly evaluate if the potential client has a pre-existing

condition, thus making the process technically legal while having

practically identical results as if they violated the restriction

under the ACA.

While this loophole has existed in the past, it is incredibly

more prominent today than ever due to the extensive development done

with genetic testing technology in recent decades (Rodriguez-Rincon

2022). Almost anyone can get their hands on a genetic test and for

much cheaper than it used to cost. Because of this outstanding influx

in the percentage of the population taking genetic testing, there is

now an incredibly large amount of data available to other genetic

testing providers. By taking a genetic test, an individual not only

gives their provider access to all the information relating to their

genome, but also information on notable statistics such as medical

conditions, medical history, age, sex, ethnicity, and geographical

location. All of this data is collected and inputted into databases.

While these databases have existed for a substantial amount of time,

they have not had nearly as much data available as they do now.

Because of this, the data available can be compiled into numerous

Genome-Wide Association Studies (GWAS) which are ever more accurate

and more developed than before.

Importantly, with the increase in data from GWAS available,

that information is now also accessible to health insurance agencies.

One important thing to note is that how insurers determine their

rates is generally very unknown. Because of this, health insurance

providers could be using the information provided by Genome-Wide

Association Studies to calculate their rates, and it would be unknown

to the public. Additionally, along with data from GWAS, insurers

likely compile other medical and genetic information such as through

screening panels, rates of conditions by demographic, and other

similar data, all of which are publicly available, to get a very

informative and statistically accurate understanding of how

predisposition to developing various conditions varies by

demographic. Nevertheless, this information is all related to the

rates of the genetic diseases themselves, which is what this study

used as data to research whether insurance agencies are performing

the previously described procedure. By taking the data from the rates

of several conditions and analyzing their correlation with health

insurance rates by geographic location, the level of correlation will

reveal the likelihood and extent to which insurance providers are

using the listed information to determine their rates.

Procedure

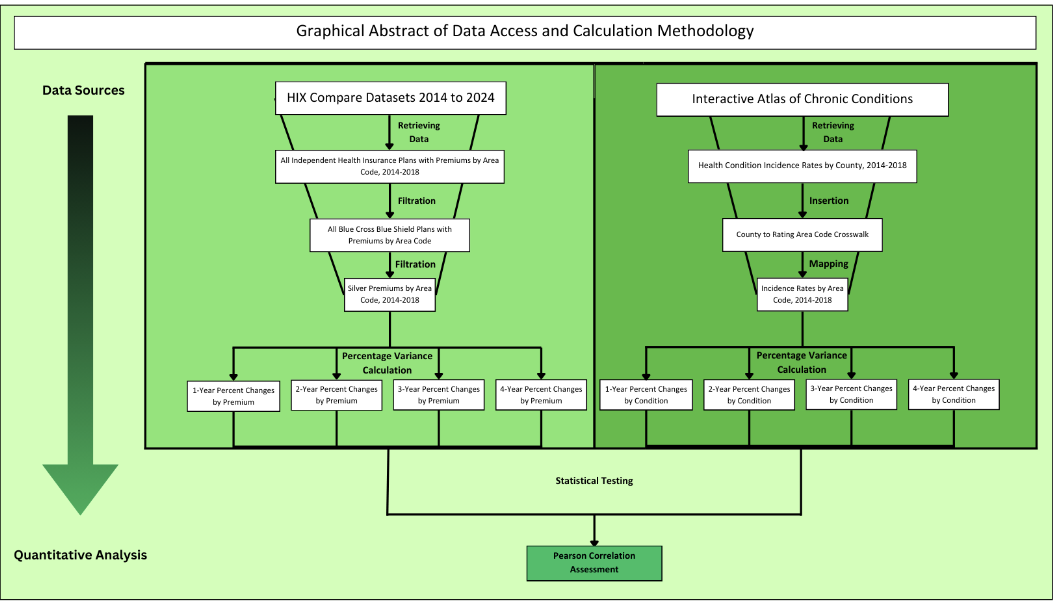

The health exchange data website, HIX Compare, has publicly

accessible reports on health plans by health insurance rate area, as

well as crosswalk datasets between health insurance rates and county.

This resource is updated annually, so this source was used to obtain

the average silver plan premium by county from 2014 to 2018. Data

obtained from this resource was compiled and stored in one large

spreadsheet.

Numerous reports, studies, and organizations have publicly

accessible data on rates of health conditions by county in the United

States. This study obtained data from numerous reports, such as the

National Cancer Institute’s State Cancer Profiles, which models the

incidence rates of cancers by county from 2016 to 2020. Similarly,

the Institute for Health Metrics and Evaluation provides a report on

the Mortality rates of diseases such as sexually transmitted

infections, diabetes and kidney disorders, and non-health related

injuries from 2000-2019. This report also used national atlases, such

as the Center for Disease Control and Prevention’s Interactive Atlas

of Heart Disease and Stroke in 2019 and the Centers for Medicare &

Medicaid Services annual reports from 2007-2018 on Chronic

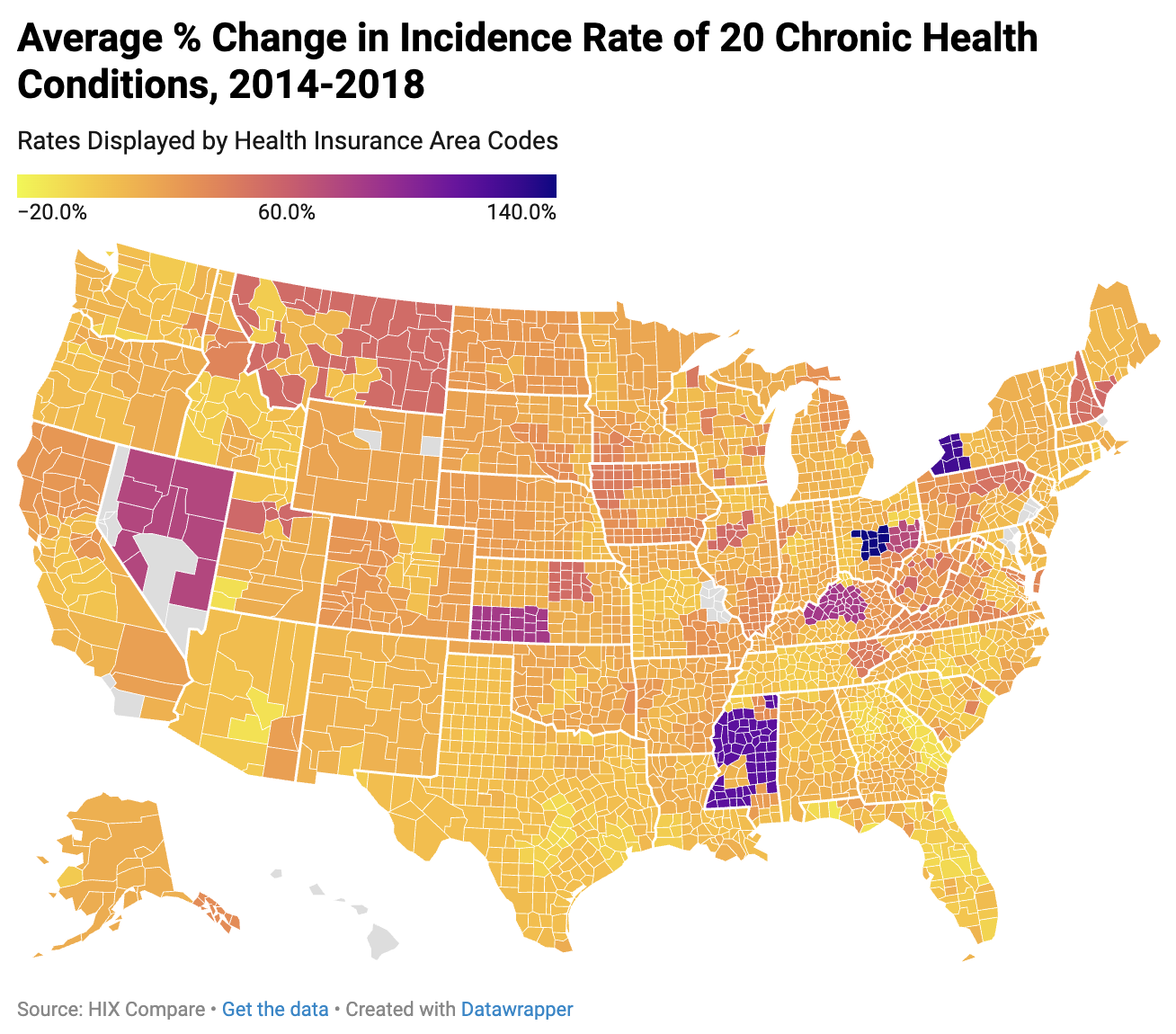

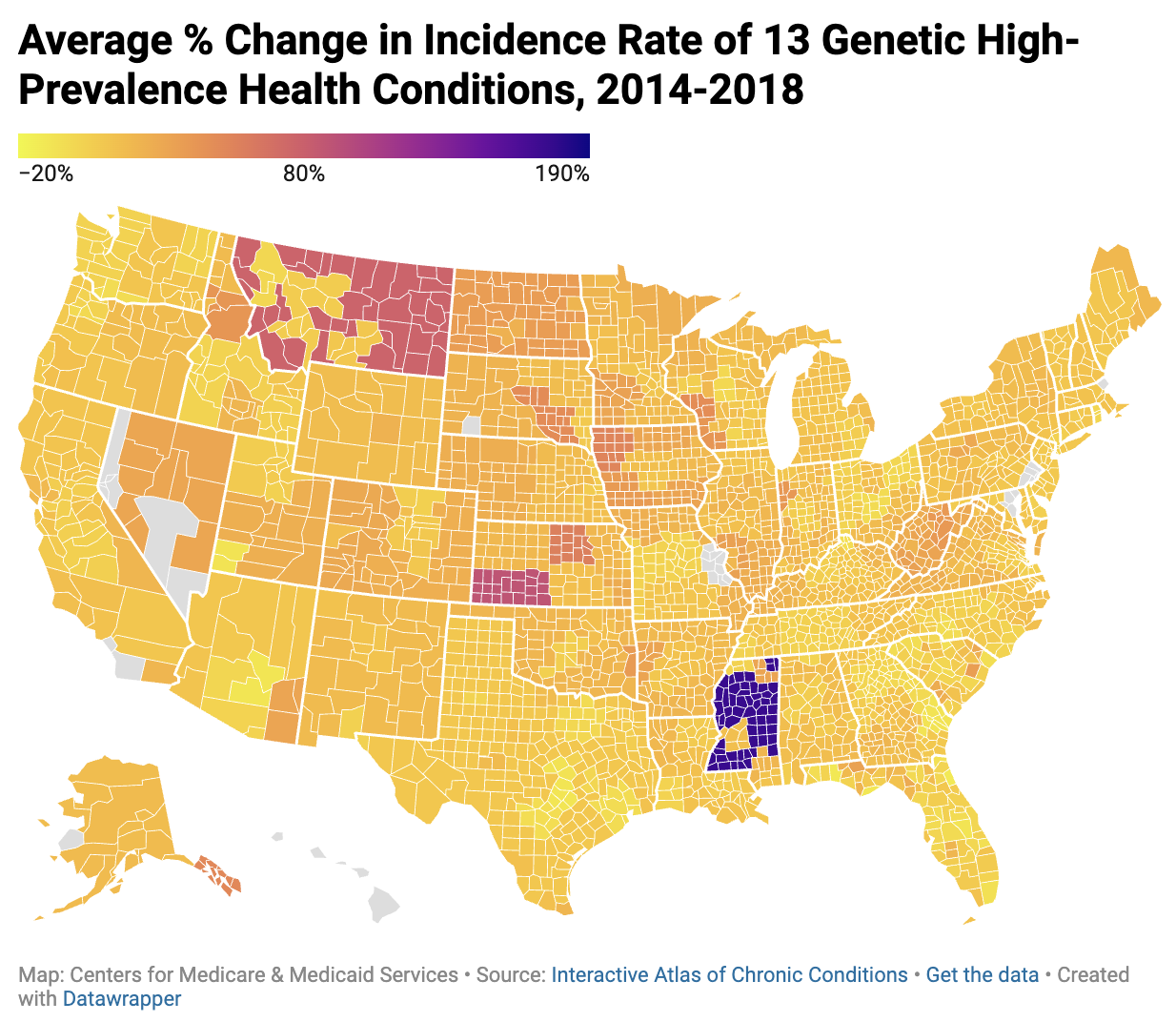

Conditions. For a preliminary model, this system utilized annual

reports on Chronic Conditions as health condition datasets.

As mentioned above, the health insurance data collected was

displayed by the health insurance area, whereas the health condition

data was collected by county. To be able to map the data, a dataset

of rates by county had to be obtained. Conversely, the most accurate

Pearson Correlation depended upon having datasets of rates by health

insurance area. For these reasons, using the previously provided

crosswalk dataset, datasets were converted such that there was a

dataset of health insurance rates and health condition incidence

rates by county as well as by health insurance rate area. This

calculation was performed in Google Sheets using the “IF”,

“REGEXMATCH”, “XLOOKUP”, and other functions provided by the

software.

While there are other factors considered in health insurance

cost calculations, this study identified smoking and state-by-state

differences as two primary external factors from health rates as

contributors in health insurance price calculations. However, whether

the client is smoking is asked and considered in the premium

calculation process. Therefore, differences in rates of smoking by

county are not considered in premium calculation. Conversely,

state-by-state differences in policy, as well as the environment, are

not avoided by this; a great portion of how much one’s health

insurance costs depends upon their state rather than their county.

Therefore, intending to avoid this, this study correlated the amount

of change over the years in percent difference. By eliminating

smoking and state-by-state policies, this study created a more

accurate and predictive model. Finally, rather than investigating the

lowest policy by the state as many popular models do, this study

decided to utilize one health insurance plan to project how one plan

in particular changes as health condition incidence rates are

adjusted, choosing to only utilize Silver-Tiered Blue Cross Blue

Shield Plans, as it is one of the more popular providers, spanning

over 20 states. There are many advantages of this approach in

comparison to using the lowest rate. For one, it will eliminate the

variable that different health insurance providers are using

different data to determine their rates. This benefit in turn enables

the study to determine exactly what factors are used for each plan.

Conversely, a negative of this approach is in increasing the demand

for datasets included if the goal is to gain an understanding of all

health insurers. However, this model functions solely as a more

preliminary study, so it does not necessarily require this. See below

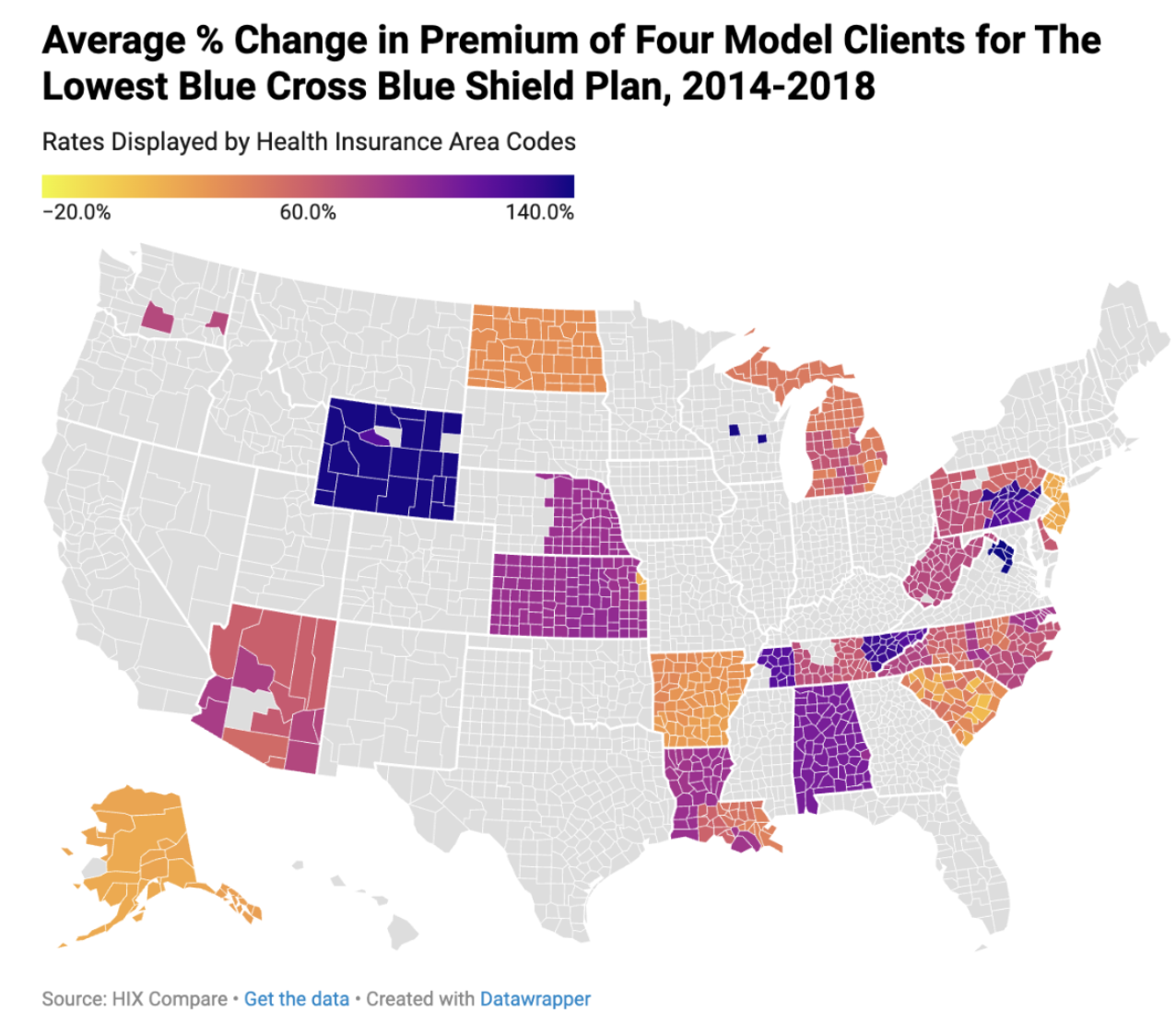

for maps of the data obtained from this process created using

Datawrapper.

Analysis

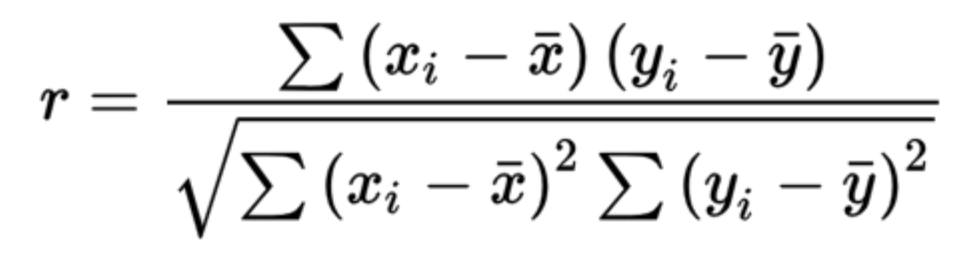

A Pearson Correlation Assessment was used as a statistical test

for this study. A Pearson correlation is a form of a linear

regression model that assesses the degree to which two sets have a

correlation with each other, reflected by a coefficient (R) from -1

to 1. A Pearson Correlation was run for each health condition in

relation to the average health insurance premium by county.

Based on the calculations run above, this study found an

average Pearson coefficient value of r = 0.1198 (See Table 1 for full

data). However, of the 13 conditions chosen with high prevalence and

genetic mutations associated with their prevalence, there was a

Pearson coefficient value of r = 0.1464.

Discussion

While it is known that a Pearson value less than or equal to

0.5 is not statistically significant evidence for a correlation, this

study is rather a comparison of Pearson coefficients. Given that

there is a larger correlation coefficient for one health condition

with health insurance premiums than another, there will be a greater

overall correlation between the first two than the second.

As this model analyzed is a preliminary version, there are

several limitations to the design that should be taken into account.

For one, the amount of data that this study was able to compile for

statistical testing became exponentially limited as mapping health

insurance plans was undergone. To avoid this, this model may be

expanded into considering additional plans rather than one, along

with adding more health condition incidence rates to create a more

informed final result.

This study expands upon several preexisting studies to go about

answering its central question of “How do health insurance companies

determine their rates?” One study which a great portion of the idea

for this project stems from is “Assessing the Impact of Developments

in Genetic Testing on Insurers’ Risk Exposure” by Rodriguez-Rincón

et. al., 2022. As a study investigating a very closely related

problem from the perspective of insurers, it had a significant impact

on the development of this study.

Following expanding this model for more insurance plans and/or

health conditions, if there is sufficient preliminary evidence

gathered from this initial model, the results of this study could be

used as significant evidence for running a similar study using

genetic predisposition rates.

Conclusion

The goal of this study was to identify differences and

similarities among health conditions in their correlation with health

insurance rates by county. By collecting and normalizing data, and

then running a Pearson Correlation on each dataset, it was observed

that there were higher correlation values among genetic conditions

than non-genetic ones. Following this study, there is sufficient

evidence promoting further research of this trend using genetic

predisposition data.