Abstract

Graphical Abstract

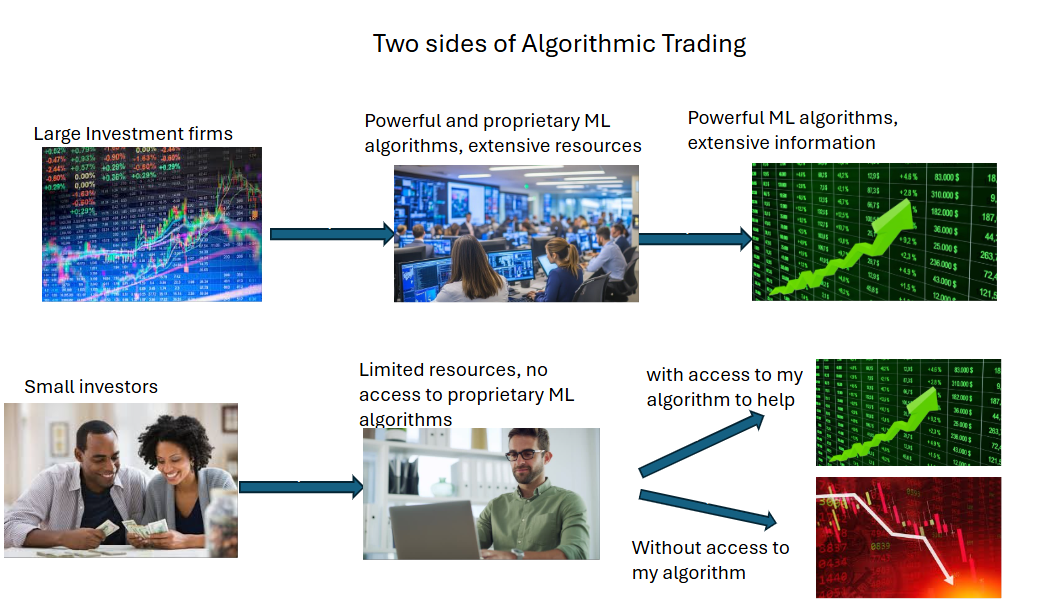

The stock market is a difficult place to survive for smaller investors, with constant competition

against far larger entities. A particular issue that many smaller investors struggle with is the lack of

access to effective, understandable, and flexible algorithms. In the new age of the stock market where

the largest investors have incredibly complex machine learning algorithms to aid their investing, making

active investment difficult for minor players. To address this issue, I will be attempting to develop an

algorithm geared toward smaller investors that will outperform the basic algorithms available today and

give a chance for smaller investors to participate in the market on a more equal footing. Previously, the

algorithm designed for smaller investors was buy and hold, which has been shown to be flawed by new

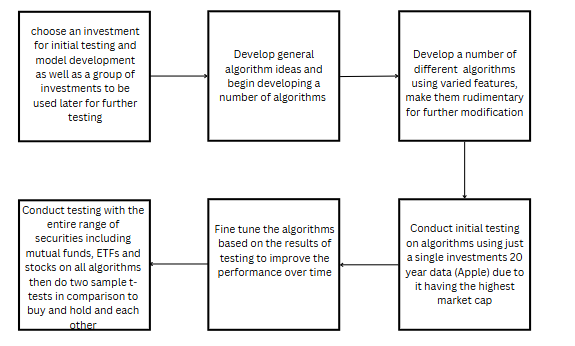

research. We will develop algorithms using historical data for testing and attempting different

approaches for algorithm development, including utilizing moving averages and the change in price. So

far, the focus has been on developing very fundamental algorithms, one of which was able to

outperform buy and hold by about 13% over the course of 20 years in initial testing which is an

encouraging sign. The goal is to combine these techniques and others to create algorithms that can be

better than buy and hold by a statistically significant margin over many stocks, ETFs and funds. By

developing this versatile algorithm, we will aid small investors in remaining competitive in today's

market.

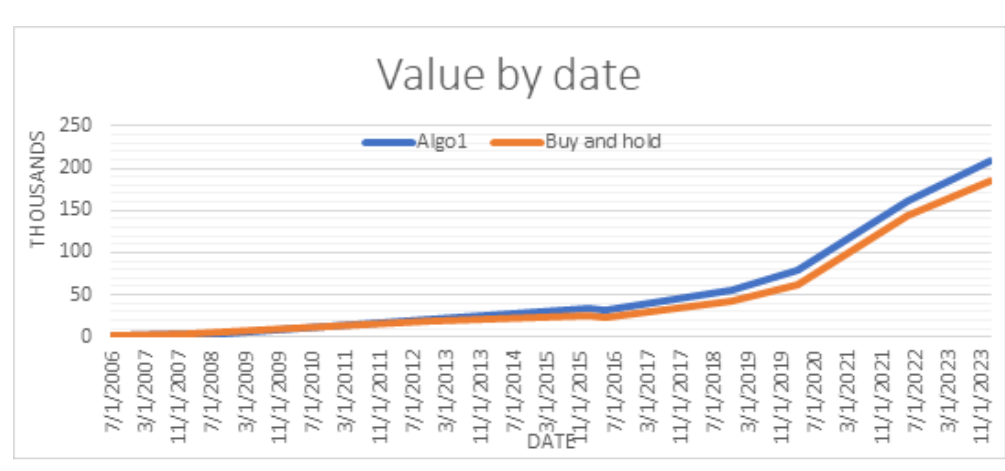

Figure 1: This is an example of the work of the justma algorithm over the entire time frame of about 20 years on the Apple stock.

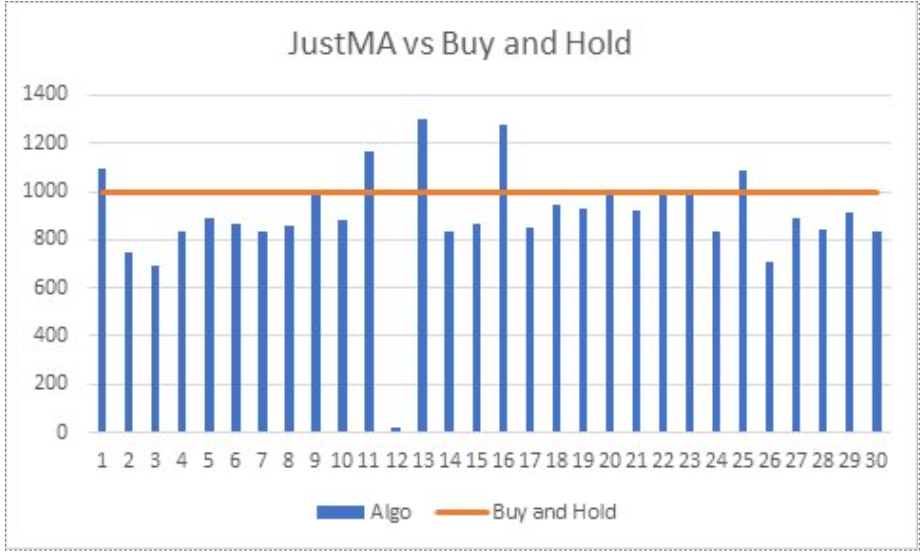

Figure 2: This is a chart of the performance of the justma algorithm on the entire dataset of stocks, ETFs, and funds that were tested.

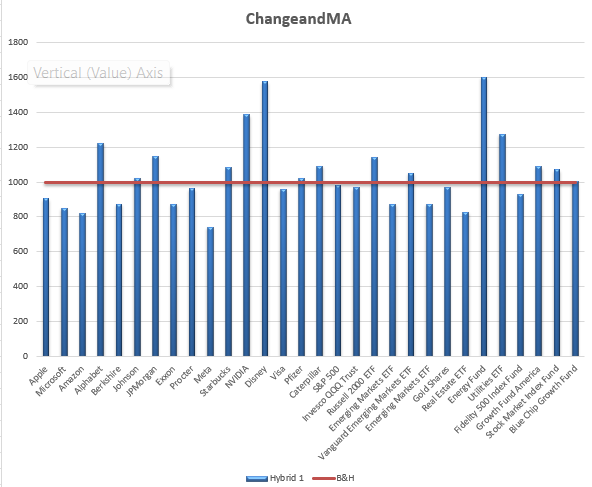

Figure 3: This is a chart of the performance of the ChangeandMA algorithm, the first hybrid developed algorithm, on the entire dataset of stocks, ETFs, and funds that were tested.

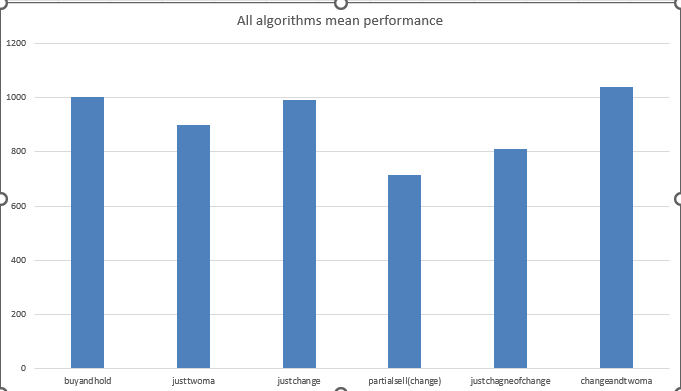

Figure 4: This is a comparison of all the algorithms that were developed which demonstrates their average performance.

Conclusion

The initial goals of this project were to develop algorithms for small investors which were easy to understand, flexible, and were able to outperform buy and hold. This is a crucial issue now more than ever, as the market has become much more perilous

for small investors, with buy and hold no longer as safe of a strategy. To address this issue, I used historical data from some of the highest cap stocks, ETFs and mutual funds to find algorithms that will be able to effectively invest in the market.

I used a variety of different features about the price of the stock, importantly avoiding any machine learning in my work and making a single generalizable algorithm. I feel like my my work has demonstrated the validity of my development process and the fact that

this algorithm can be applied to the current time period with results that won't suffer due to overfitting. More importantly, I was able to develop an algorithm without using machine learning that was easy to understand and flexible, and which outperformed buy and hold.

As much as this project was meant to produce a successful algorithm, it was also meant to show the viability of this kind of algorithm development to encourage others to consider this idea, as well as giving access to a baseline successful algorithm to give small investors

an idea of what might work.

References

Ayyildiz, N., & Iskenderoglu, O. (2024). How effective is machine learning in stock market predictions? Heliyon, 10(2). https://doi.org/10.1016/j.heliyon.2024.e24123

Chen, J. (2024). Algorithmic trading: Definition, how it works, pros & cons. Investopedia. https://www.investopedia.com/terms/a/algorithmictrading.asp

Chen, C., Chen, C., & Liu, T. (2020). Investment performance of machine learning: Analysis of S&P 500 Index. International Journal of Economics and Financial Issues, 10(1). https://www.econjournals.com/index.php/ijefi/article/download/8925/pdf/21843

Huang, W., Satoru, G., & Nakamura, M. (2021). Decision-making for stock trading based on trading probability by considering whole market movement. European Journal of Operational Research, 157(1), 227-241. https://doi.org/10.1016/S0377-2217(03)00144-9

Huang, Y., Zhou, C., Cui, K., & Lu, X. (2024). Improving algorithmic trading consistency via human alignment and imitation learning. Expert Systems with Applications, 253, 124350. https://doi.org/10.1016/j.eswa.2024.124350

Kuo, S.-Y., & Chou, Y.-H. (2021). Building intelligent moving average-based stock trading system using metaheuristic algorithms. IEEE Access, 9, 140383-140396. https://doi.org/10.1109/ACCESS.2021.3119041

Ling, F., Ng, D., & Muhamad, R. (2014). An empirical re-investigation on the 'buy-and-hold strategy' in four Asian markets: A 20 years' study. World Applied Sciences Journal, 30(30). https://doi.org/10.5829/idosi.wasj.2014.30.icmrp.30

Picardo, E. (2024). Investing explained: Types of investments and how to get started. Investopedia. https://www.investopedia.com/terms/i/investing.asp

Qin, L. (2018). Game theory-based investment strategy vs. buy-and-hold: Which optimizes profits? ISEF Abstracts. https://abstracts.societyforscience.org/Home/FullAbstract?ISEFYears=0%2C&Category=Any%20Category&Finalist=Qin&AllAbstracts=True&FairCountry=Any%20Country&FairState=Any%20State&ProjectId=16428

Saez, E., & Zucman, G. (2020). The rise of income and wealth inequality in America: Evidence from distributional macroeconomic accounts. Journal of Economic Perspectives, 34(4), 3-26. https://doi.org/10.1257/jep.34.4.3

Sakhare, A., Mhaskar, N., Mishra, V., & Chavan, M. (2021). Algorithmic trading for a buy-sell platform: Study and comparison. ITM Web of Conferences, 40, 03020. https://doi.org/10.1051/itmconf/20214003020

Sanderson, R., & Lumpkin-Sowers, N. (2018). Buy and hold in the new age of stock market volatility: A story about ETFs. International Journal of Financial Studies, 6(3). https://doi.org/10.3390/ijfs6030079

Sikalo, M., Arnaut-Berilo, A., & Zaimovic, A. (2022). Efficient asset allocation: Application of game theory-based model for superior performance. International Journal of Financial Studies, 10(1), 20. https://doi.org/10.3390/ijfs10010020

Sobolev, D., Chan, B., & Harvey, N. (2017). Buy, sell, or hold? A sense-making account of factors influencing trading decisions. Cogent Economics & Finance, 5. https://doi.org/10.1080/23322039.2017.1295618

Taylor, B. (2024). 5 key investment strategies to learn before trading. Investopedia. https://www.investopedia.com/investing/investing-strategies/